The American healthcare industry generates more than $4.8 trillion in annual spending, yet most rankings of the top healthcare providers in the US rely on a single metric. Some count beds. Others sort by revenue. A few rank on reputation surveys alone. Honestly, those one-dimensional lists tell only part of the story. A health system operating 190 hospitals with average patient experience scores is not the same kind of leader as one operating 33 hospitals where patients rate their care among the best in the world.

That distinction matters because the healthcare organizations shaping patient outcomes today are not simply the largest. They are the ones blending operational scale with clinical excellence, digital innovation, and sustainable financial performance simultaneously. Therefore, this analysis applies a multi-dimensional scoring model that normalizes across fundamentally different organizational structures: investor-owned systems, nonprofit networks, integrated payer-provider organizations, and academic medical centers.

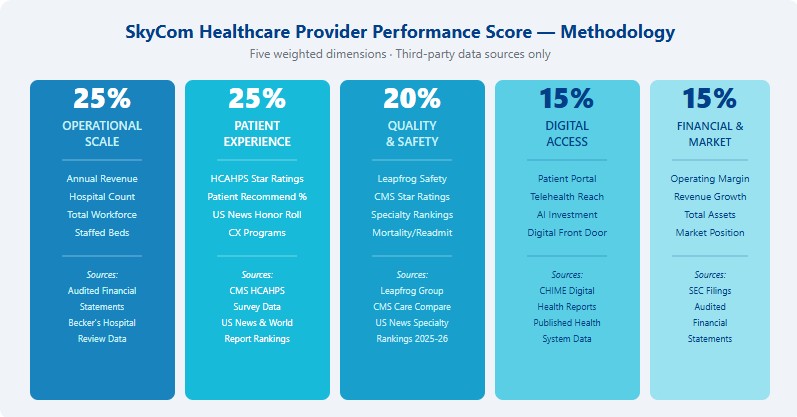

The SkyCom Healthcare Provider Performance Score weights five measurable dimensions. Data comes from CMS, The Leapfrog Group, U.S. News & World Report, audited financial statements, and HCAHPS survey data. The result is a defensible composite that rewards balanced excellence rather than pure size.

Why Size Alone Does Not Define a Leading Healthcare Provider

Revenue is the default sorting criterion in most healthcare rankings, and it distorts reality in predictable ways. Kaiser Permanente’s $127.7 billion in 2025 operating revenue dwarfs every other health system in the country. But that figure includes premium revenue from 13.1 million health plan members, a revenue stream that HCA Healthcare, Cleveland Clinic, and Mayo Clinic do not collect because they are not insurance companies. Comparing Kaiser’s topline to a pure-play hospital system is like comparing a grocery chain’s total revenue to a restaurant’s food sales. The numbers exist in fundamentally different economic structures.

Similarly, HCA Healthcare operates 190 hospitals across 20 states, making it the largest for-profit hospital company in the world by any measure. Yet the Leapfrog Group consistently shows that scale and safety are not synonymous. Among the 11 hospitals that earned straight-A Leapfrog Safety Grades for all 27 consecutive grading rounds over 13 years, most belong to mid-sized or regional systems rather than national giants.

Then there is Mayo Clinic. Its $21.5 billion in 2025 revenue places it ninth among the systems analyzed here, but it leads the U.S. News & World Report Best Hospitals Honor Roll for the 36th time. Mayo is the only organization among the top 20 Honor Roll hospitals to hold a 5-star HCAHPS rating. That kind of patient experience excellence, sustained across decades, represents a form of leadership that revenue alone cannot capture.

These structural differences demand a scoring model that normalizes across system types. The SkyCom Healthcare Provider Performance Score does exactly that.

Methodology: The SkyCom Healthcare Provider Performance Score

The scoring model evaluates each health system across five weighted dimensions. Every input comes from publicly available, third-party data sources. No proprietary surveys, no self-reported claims, no subjective editorial judgment.

Operational Scale (25%) measures the system’s physical footprint: annual revenue, hospital count, staffed beds, and total workforce. Patient Experience (25%) draws from CMS HCAHPS star ratings, patient recommendation percentages, and U.S. News recognition. Quality & Safety (20%) incorporates Leapfrog Hospital Safety Grades, CMS overall star ratings, and specialty rankings. Digital Access (15%) evaluates patient portal maturity, telehealth capabilities, and AI investment. Financial & Market Strength (15%) assesses operating margins, revenue growth trajectories, and balance sheet stability.

Why give Patient Experience equal weight to Operational Scale? Because HCAHPS data from CMS consistently shows that patient experience scores correlate with readmission rates, clinical outcomes, and malpractice risk. Health systems that patients would recommend to friends and family tend to deliver measurably better clinical outcomes across every specialty. The weighting reflects that correlation.

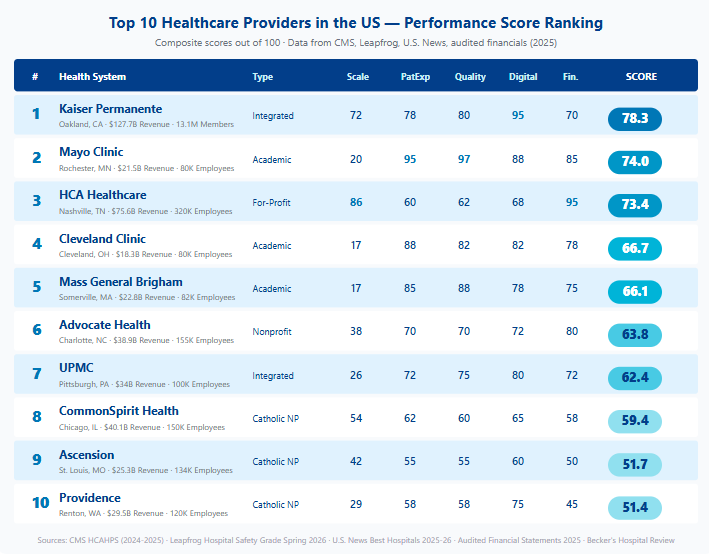

The Complete Top 10 Ranking: SkyCom Healthcare Provider Performance Scores

The ranking reveals something most industry observers already suspect but rarely see quantified. The three academic medical centers — Mayo Clinic, Cleveland Clinic, and Mass General Brigham — punch dramatically above their weight relative to their revenue. Meanwhile, the three Catholic nonprofit systems — CommonSpirit, Ascension, and Providence — face a consistent gap between operational scale and the patient experience and quality metrics that define clinical leadership.

1. Kaiser Permanente — Score: 78.3

Kaiser Permanente tops the ranking not because it is the largest, although its $127.7 billion in 2025 operating revenue makes it the nation’s highest-revenue health system. Kaiser leads because its integrated payer-provider model produces structural advantages in every dimension of the scoring model simultaneously.

The organization combines health plan operations serving nearly 13.1 million members with 55 hospitals and 847 medical offices across 9 states and the District of Columbia. That integration means Kaiser controls both the care delivery and the financing of care — a structural alignment that enables investments in preventive medicine and population health management that fee-for-service systems cannot easily replicate.

Kaiser earned a Digital Access score of 95, the highest in the ranking. Its patient portal and digital health tools serve millions of virtual interactions annually. Kaiser Permanente’s Orange County-Anaheim Medical Center is one of just 11 hospitals nationwide to earn straight-A Leapfrog Hospital Safety Grades for every grading round since the program began in 2012, spanning 13 consecutive years of sustained safety excellence.

What Healthcare Leaders Can Learn: Kaiser’s dominance reflects the compounding advantage of structural integration. When the insurer and the provider are the same organization, every dollar spent on prevention reduces future claims costs. That alignment drives investments in patient access, scheduling systems, and care coordination infrastructure that fragmented systems simply cannot justify on the same timeline.

2. Mayo Clinic — Score: 74.0

Mayo Clinic recorded the highest Patient Experience and Quality & Safety scores in the entire ranking — 95 and 97, respectively — on $21.5 billion in 2025 revenue that places it ninth in the scale dimension. That gap between scale and quality is precisely the story this scoring model was built to tell.

Mayo earned a record $1.5 billion in operating income in 2025, its strongest financial year to date. Both its Rochester and Arizona campuses made the U.S. News & World Report Best Hospitals Honor Roll for 2025-2026 — the only health system with two hospitals earning that distinction. Mayo led the rankings for the 36th time since the program’s inception, and it is the only organization among the top 20 Honor Roll hospitals with a 5-star HCAHPS rating, according to Mayo’s chief value officer.

Six of Mayo’s 11 eligible hospitals earned 5-star CMS overall quality ratings, and Mayo Clinic-Phoenix holds one of the 11 all-time straight-A Leapfrog Safety designations since 2012. The system also leads in 13 nationally ranked specialties, including gastroenterology, endocrinology, and orthopedics.

What Healthcare Leaders Can Learn: Mayo proves that a physician-led, referral-based model can deliver world-class financial returns alongside the best patient experience scores in the country. The lesson for every health system executive is that patient experience and financial performance are not trade-offs. They are reinforcing investments that compound over decades, not quarters.

3. HCA Healthcare — Score: 73.4

HCA Healthcare is the most financially dominant health system in America. Its $75.6 billion in 2025 revenue, $11.97 billion in operating income, and 16.5% operating margin make it the benchmark for operational efficiency at scale. With 190 hospitals and 320,000 employees across 20 states and England, HCA also leads in Operational Scale with a score of 86.

However, the Financial & Market Strength score of 95 is counterbalanced by more modest performance in Patient Experience (60) and Quality & Safety (62). Operating 190 hospitals with consistent quality and satisfaction scores is an enormous challenge. HCA’s patient experience performance varies significantly across its American, Atlantic, and National geographic groups. That variability is a structural consequence of the for-profit model’s focus on acquisition-driven growth and margin optimization.

HCA’s 2025 admissions grew 2.7% on a consolidated basis and 2.3% on a same-facility basis, with emergency room visits increasing 1.6%. Revenue per equivalent admission rose 4%, reflecting continued pricing power. The system is projecting revenue between $76.5 billion and $80 billion in 2026.

What Healthcare Leaders Can Learn: HCA demonstrates that financial discipline and operational scale can coexist, but only if patient experience investments keep pace with growth. The widening gap between HCA’s margin leadership and its patient experience metrics represents a strategic risk that forward-thinking health systems should study carefully.

4. Cleveland Clinic — Score: 66.7

Cleveland Clinic earned 13 national specialty rankings and the highest possible rating in 21 of 22 U.S. News procedures and conditions for 2025-2026. Its cardiology program consistently ranks among the top three nationally. The system posted $18.3 billion in 2025 revenue with a 5% operating margin and $913 million in operating income, reflecting strong financial performance for an academic medical center.

Cleveland Clinic pioneered the formal patient experience function in American healthcare, creating the nation’s first Chief Experience Officer position. That organizational commitment shows in its Patient Experience score of 88, second only to Mayo Clinic. The system’s approach to patient experience has become a model studied by health systems worldwide.

Quality performance is nuanced. While the Cleveland Clinic main campus has faced mixed Leapfrog Safety Grades, its regional hospitals including Fairview, Marymount, and Hillcrest earned A grades in the spring 2026 assessment. Total assets of $29.6 billion provide strong balance sheet backing for continued investment.

What Healthcare Leaders Can Learn: Cleveland Clinic’s journey demonstrates that patient experience transformation requires organizational commitment at the C-suite level. Creating a Chief Experience Officer position was not a symbolic gesture — it was a structural decision that embedded patient-centricity into clinical operations, provider engagement models, and staff training protocols across the system.

5. Mass General Brigham — Score: 66.1

Mass General Brigham, the academic health system built around Massachusetts General Hospital and Brigham and Women’s Hospital, posted $22.8 billion in revenue for the 12 months ending September 2025. Both flagship hospitals made the U.S. News Honor Roll, with Brigham and Women’s ranked first nationally in obstetrics and gynecology and third in both cancer care and endocrinology.

The system holds $35.8 billion in total assets, the fifth-highest among all U.S. health systems, reflecting decades of research endowment growth. Mass General Brigham’s research enterprise produces more NIH-funded research than nearly any other hospital system in the country. That research intensity directly translates into clinical innovation and specialty care quality, earning a Quality & Safety score of 88.

Its scale limitation (16 hospitals, 82,000 employees) explains the lower Operational Scale score of 17. Mass General Brigham deliberately chose depth over breadth, concentrating resources in the Greater Boston corridor rather than pursuing national expansion through acquisitions.

What Healthcare Leaders Can Learn: Regional concentration with world-class depth can outperform broad geographic scale on every quality and patient experience metric. Mass General Brigham’s model challenges the assumption that health system growth must mean geographic expansion.

6. Advocate Health — Score: 63.8

Advocate Health, formed from the 2022 merger of Advocate Aurora Health and Atrium Health, posted $38.9 billion in 2025 revenue with a 4% operating margin and $1.5 billion in operating income. With 69 hospitals and approximately 155,000 employees across the Midwest and Southeast, Advocate represents the new generation of mega-system mergers that reshaped the healthcare landscape.

The system holds $54.6 billion in total assets, the second-highest among all U.S. health systems after Kaiser Permanente. That balance sheet strength positions Advocate for continued strategic investment, though the patient experience integration challenge remains ongoing. Merging two large systems with different clinical cultures, EHR platforms, and care delivery models takes years to fully harmonize.

Advocate’s financial trajectory represents the greatest year-over-year improvement among the top 10 systems, with net patient revenue growing 11.8% from 2024 to 2025, the highest growth rate in the ranking.

What Healthcare Leaders Can Learn: Post-merger integration determines whether a health system merger creates value or merely creates scale. Advocate’s story is still being written, but the early financial indicators suggest disciplined execution on operational synergies.

7. UPMC — Score: 62.4

UPMC’s integrated model pairs a 40-hospital health system with a health insurance division serving more than 4.1 million members across employer-sponsored, Medicare Advantage, Medicaid, and ACA plans. The system recorded approximately $34 billion in total revenue in 2025, with insurance enrollment revenue reaching $17.6 billion alone.

UPMC demonstrated the most dramatic financial turnaround in the ranking, posting a $625 million improvement in operating performance from 2024 to 2025. Net income rebounded to $635.4 million, compared to a net loss of $14.7 million the prior year. The turnaround was driven partly by improved insurance underwriting margins, with the health plan’s medical loss ratio declining to 91%.

UPMC earned a Digital Access score of 80, reflecting substantial investments in clinical AI, research computing, and its MyUPMC patient engagement platform. The system’s academic affiliation with the University of Pittsburgh drives clinical innovation across transplant, oncology, and neuroscience programs.

What Healthcare Leaders Can Learn: The payer-provider integration model pioneered by Kaiser Permanente can work outside California. UPMC proves that mid-Atlantic and Midwestern health systems can build sustainable integrated models when insurance operations and clinical delivery share strategy, data, and incentives.

8. CommonSpirit Health — Score: 59.4

CommonSpirit Health is the nation’s largest Catholic health system and the third-largest by total operating revenue at $40.1 billion for the 12 months ending June 2025. Formed from the 2019 merger of Catholic Health Initiatives and Dignity Health, CommonSpirit operates 158 hospitals across 21 states, the second-largest hospital count behind HCA Healthcare.

The system’s Operational Scale score of 54 reflects its massive physical footprint and workforce. However, CommonSpirit’s patient experience and quality scores lag behind both the academic medical centers and the integrated systems in this ranking. The challenge of maintaining consistent quality across 158 hospitals spanning diverse geographic markets — from dense urban centers to rural communities — is structurally different from managing a concentrated regional system.

CommonSpirit reported a 1.8% increase in net patient revenue from 2024 to 2025, demonstrating steady growth albeit at a slower pace than peers like Advocate Health.

What Healthcare Leaders Can Learn: Mission-driven healthcare delivery at massive scale requires systematic investment in the operational infrastructure that supports clinical quality: standardized insurance verification workflows, consistent scheduling protocols, and revenue cycle processes that free clinicians to focus on care delivery rather than administrative complexity.

9. Ascension — Score: 51.7

Ascension operates 119 hospitals across 16 states, making it one of the largest Catholic nonprofit health systems in the country. The system reported $25.3 billion in revenue for the 12 months ending June 2025, alongside $39.9 billion in total assets. However, Ascension experienced a 12.9% decline in net patient revenue between 2024 and 2025, the sharpest contraction among the top 10 systems.

That decline was driven primarily by deliberate hospital divestitures and portfolio restructuring rather than weakening same-facility performance. Ascension has been strategically shedding hospitals in markets where it lacks competitive density, refocusing resources on core markets where it can achieve meaningful scale advantages. The restructuring is a rational long-term strategy, but it depressed the system’s Financial & Market Strength and Quality scores during the transition period.

Ascension has faced additional operational challenges, including a significant cybersecurity incident in 2024 that disrupted clinical operations across multiple facilities and underscored the vulnerability of large health systems to digital threats.

What Healthcare Leaders Can Learn: Portfolio rationalization — choosing where not to operate — is sometimes the most strategically valuable decision a health system can make. Ascension’s willingness to divest underperforming hospitals reflects a maturity that systems clinging to every facility often lack.

10. Providence — Score: 51.4

Providence operates 51 hospitals and more than 1,000 physician clinics across seven western states, serving communities from Alaska to Texas. The system reported $29.5 billion in total operating revenue for 2025, up from $28.1 billion the prior year, with net patient service revenue reaching $24.5 billion.

Providence’s story in 2025 was one of financial turnaround. The system narrowed its operating loss to $486 million from $546 million in 2024, delivering two consecutive quarters of positive operating margin in the second half of the year. The system cited increased patient volumes, improved labor productivity from reducing temporary agency staffing, and disciplined cost management as the primary drivers of improvement.

Providence earned a Digital Access score of 75, reflecting its investments in Providence DXP, a digital front-door platform designed to simplify patient access across its sprawling multi-state network. The system’s leadership has emphasized that digital transformation is central to its operational turnaround strategy.

What Healthcare Leaders Can Learn: Financial turnarounds in healthcare require sustained operational discipline across multiple quarters, not single-quarter heroics. Providence’s trajectory demonstrates that cost management, volume growth, and workforce optimization must all move in the same direction simultaneously for a turnaround to become durable.

What the Top 10 Reveal About Healthcare Operations in America

Looking across all ten systems, several patterns emerge that should matter to any healthcare executive thinking about long-term competitive positioning.

First, the integrated payer-provider model produces the most consistently high composite scores. Both Kaiser Permanente and UPMC operate insurance arms alongside their clinical delivery systems. That integration aligns financial incentives in ways that pure-play hospital systems cannot replicate. When the payer benefits from lower utilization and the provider benefits from higher quality, the system naturally invests in exactly the preventive care, care coordination, and patient access infrastructure that drives better outcomes.

Second, academic medical centers consistently outperform their scale on quality and patient experience. Mayo Clinic, Cleveland Clinic, and Mass General Brigham each scored in the top five on Patient Experience and Quality & Safety despite ranking eighth, tenth, and eleventh, respectively, by revenue among all U.S. health systems. Their physician-led governance structures, research intensity, and selective patient populations create environments where clinical excellence is the primary strategic priority rather than volume growth.

Third, the three Catholic nonprofit systems in the ranking — CommonSpirit, Ascension, and Providence — share a common challenge. Their mission-driven commitment to serving vulnerable populations creates operational complexity that investor-owned systems can avoid. They operate in markets where payer mix includes higher proportions of Medicaid and uncompensated care. That mission is essential to American healthcare, but it creates structural headwinds for patient experience and financial performance metrics simultaneously.

Fourth, and perhaps most importantly for healthcare operations leaders, the systems with the strongest patient experience scores all made deliberate investments in the operational functions that shape how patients interact with the system before, during, and after clinical encounters. Patient access centers, appointment scheduling workflows, insurance verification processes, prior authorization management, claims processing efficiency, and revenue cycle operations all influence the patient experience scores that CMS publicly reports through HCAHPS.

Why Patient Access and Revenue Cycle Operations Drive Healthcare Performance

The operational patterns across these top 10 health systems reveal an underappreciated truth about healthcare performance. The clinical encounter itself — the doctor-patient interaction — accounts for only a fraction of the total patient experience that HCAHPS measures. The moments before and after the clinical encounter often determine whether a patient rates their experience as excellent or merely adequate.

Consider what a typical patient navigates before seeing a physician: calling to schedule an appointment, verifying insurance eligibility, obtaining prior authorization for a recommended procedure, navigating billing questions after the visit, resolving claims disputes, and managing payment arrangements. Each of these touchpoints is an operational function, not a clinical one. And each one directly affects both patient satisfaction scores and revenue cycle performance.

Health systems that invest in patient access center operations — ensuring that calls are answered promptly, that scheduling is streamlined, that insurance verification happens before the appointment rather than during it — consistently outperform on HCAHPS measures for communication and care coordination. Organizations like SkyCom specialize in building exactly this kind of healthcare BPO infrastructure that supports patient access, appointment scheduling, insurance verification, prior authorization, claims processing, and revenue cycle management for health systems seeking to improve both patient experience and operational efficiency.

Prior authorization alone consumes an estimated 34 hours per physician per week in administrative burden, according to American Medical Association survey data. When health systems outsource prior authorization workflows to specialized operations teams, they recover physician time for patient care while simultaneously reducing authorization turnaround times. That dual benefit — better physician satisfaction and faster patient access — compounds across every facility in a multi-hospital system.

Revenue cycle management is equally critical. The top-performing systems in this ranking all maintain days in accounts receivable below industry benchmarks and first-pass claims acceptance rates above 95%. Those metrics do not improve through clinical excellence alone. They require dedicated revenue cycle operations teams with deep expertise in payer-specific billing rules, denial management workflows, and compliance requirements that vary by state and insurance product.

Conclusion: What These Rankings Tell Healthcare Decision-Makers

The top healthcare providers in the US share three patterns that most ranking methodologies fail to capture. First, balanced excellence across clinical quality, patient experience, operational efficiency, and digital access produces more sustainable competitive advantages than dominance in any single dimension. Second, organizational structure matters enormously. Integrated payer-provider models, academic medical centers, and large Catholic nonprofit systems face fundamentally different strategic realities that single-metric rankings obscure. Third, the operational functions that sit between the patient and the clinician — access, scheduling, verification, authorization, billing, and revenue cycle management — are increasingly the differentiating factors between systems that compound advantages and those that lose ground.

Whether your organization operates 190 hospitals or 16, the evidence from these top 10 systems points in the same direction. Sustained investment in patient experience infrastructure, clinical quality systems, and the operational workflows that support both is the surest path to healthcare leadership in America.